The Upcoming PERS Crisis: The system is facing a $30 billion shortfall—radical reform is needed

By Eric Fruits, Ph.D.

Coronavirus has hit the economy hard. Nearly all the stock market gains from the past two or three years have been wiped out. While it’s painful for investors and retirees, it’s likely to fuel the third major PERS crisis since the dot-com bust.

PERS, the public employee retirement system, has two major sources of funds: investment returns and employer contributions. PERS investments are managed by the state treasurer, under guidance from the Oregon Investment Council. “Employers” are state and local governments whose employees are PERS members.

PERS charges these employers a rate equal to some percent of their payroll to fund the costs of their employees’ anticipated retirement benefits. Currently, the average rate is approximately 25% of payroll. For example, for a city employee with a salary of $60,000 a year, the city must pay an additional $15,000 to PERS.

One of the many factors that affect the employer rate is the unfunded actuarial liability, or UAL. The UAL is an estimate of how much money would be needed to pay off all existing beneficiaries if the system were liquidated. Think of it this way: If you sold everything you owned—house, car, checking, savings, retirement—would you have enough to pay everyone you owe? If you don’t, you have unfunded liabilities.

PERS currently has a UAL of $24.5 billion. If PERS liquidated all its assets to pay its existing members, the system would be $24.5 billion short. The employer rate is set to fill that gap over a period of approximately 20 years. So, if the UAL increases, the employer rate increases. Similarly, if the UAL decreases, so does the employer rate.

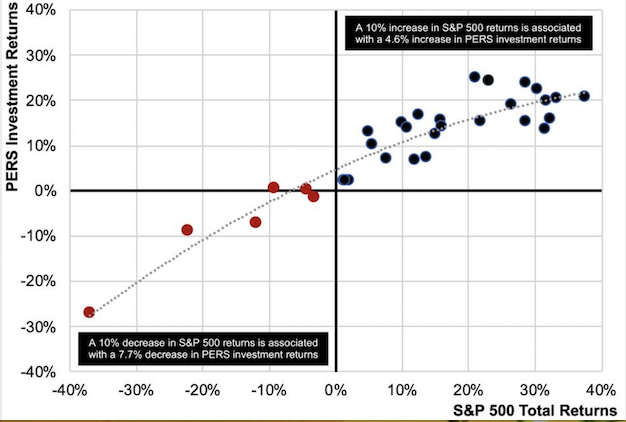

Here’s where investment returns come in.

Because of the way PERS benefits are calculated, the system’s investments must earn an average of at least 7.2% a year to stop the UAL from getting bigger. That’s a very aggressive, and optimistic, target.

In good times, when PERS investments earn above average returns, the money from the investments reduces the UAL, which in turn reduces the employer contribution rate. If, on the other hand, PERS investments tank, the UAL balloons, and state and local governments must make bigger contributions to fill the gap.

PERS investment returns are correlated with stock market returns. Generally speaking, in a bull market, PERS investments run with the bulls; when the market drops, PERS investments suffer as well.

The stock market is down more than 20% from the beginning of the year. That means PERS investments would be down by about 11%. Based on past experience, such a drop would add another $6 billion to PERS’ unfunded liabilities, for a total UAL of about $30 billion.

Let’s say the economy improves and the stock market recovers all its losses, ending the year unchanged from the beginning of the year. PERS investments would be up by about 5%, based on past experience. Even so, PERS unfunded liabilities would increase by about $3 billion for a total UAL of about $27 billion.

Based on these observations, it’s very possible that state and local governments would face an employer contribution rate for PERS of 30% or more. That $60,000 employee would now come with an $18,000 additional cost to pay for PERS.

Where will that additional money come from?

It’ll come from us. Legislators and local governments will be under tremendous pressure to raise taxes to pay for skyrocketing PERS costs. Along with that will come budget cuts, with fewer teachers, state police, foster care workers resulting in bigger class sizes, reduced law enforcement, and more children stranded in the foster system. It’s not just a financial crisis, it’s a human crisis.

PERS has been a ticking time bomb for two decades. Attempts at meaningful reform have been put off by timid politicians and thwarted by powerful public employee unions. In the first PERS crisis of 2002, the system’s unfunded liabilities were less than $4 billion. In the second crisis, beginning in 2008, the UAL ballooned to $16 billion. Today, we’re looking at a third crisis with a UAL of $30 billion or more, or nearly $19,000 per household.

We are entering an era in which PERS cannot be merely tweaked or reformed. We are entering a PERS crisis that will require a radical overhaul of the entire system. It can begin with some straightforward first steps:

- Move all new public employees into a 403(b) defined contribution plan. These are similar to the 401(k) plans held by many private sector employees. TriMet has already made the switch, and it saved the agency from insolvency.

- The PERS Board must change its assumed rate of return on PERS investments. Because of the mismatch between assumed and actual investment returns, PERS is accruing liabilities much faster than it’s growing its assets. Bad assumptions were unsustainable 20 years ago, and they’re disastrous now.

These are just first steps that can be handled quickly in an emergency session of the legislature and an emergency meeting of the PERS board. There’s never a good time to upset the public employee unions. Now that we’re in a crisis, it’s time for leadership and action to save the state from fiscal disaster.

Eric Fruits, Ph.D. is Vice President of Research at Cascade Policy Institute, Oregon’s free market public policy research organization.

Click here for PDF version: